US Corn and Soybean Ending Stocks Decrease in 2024/2025

Author

Published

4/10/2025

Introduction

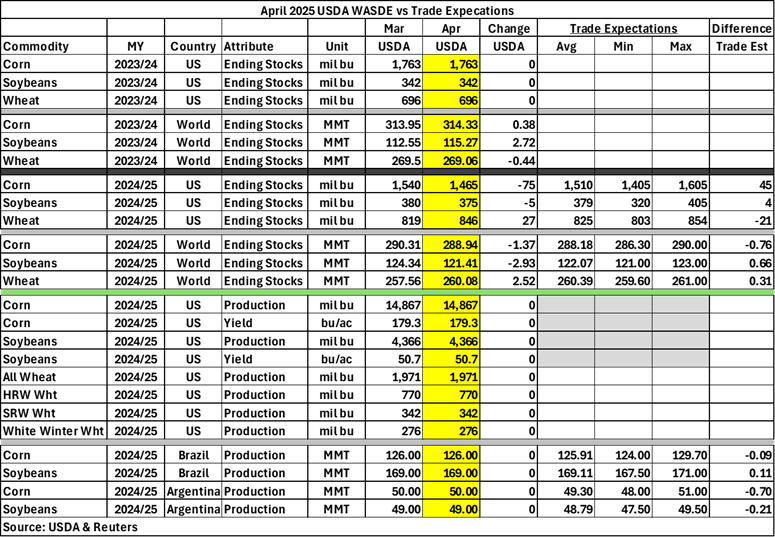

The USDA released its updated WASDE report on April 10, 2025. Compared to the March 2025 WASDE report, US wheat ending stocks increased by 27 million bushels (mb) to 846 mb while US corn and soybeans ending stocks decreased by 75 mb and 5 mb respectively. World corn and soybean ending stocks for the 2024/2025 marketing year both decreased by 1.37 MMT and 2.93 MMT respectively. World wheat ending stocks increased by 2.52 MMT.

Regarding prior year data, US corn, soybean, and wheat ending stocks remain unchanged for the 2023/2024 marketing year. Corn, soybean, and wheat production and yield estimates have stayed constant from January to April for the 2024/2025 marketing year. In the 2023/2024 marketing year, world corn and soybean ending stocks had slight increases of 0.38 million metric tons (MMT) and 2.72 MMT, while wheat ending stocks decreased by 0.44 MMT.

Table 1 shows some key report estimates along with trade analyst expectations.

Table 1. April 2025 USDA WASDE vs Market Expectations

US corn and soybean ending stocks were less than trade expectations by 45 mb and 4 mb respectively for the 2024/2025 marketing year. US wheat ending stocks exceeded expectations by 27 mb for the 2024/2025 marketing year. World corn ending stocks for the 2024/2025 marketing year were slightly below trade expectations by 0.76 MMT, while world soybean and wheat ending stocks for the 2024/2025 marketing year were above trade expectations by 0.66 MMT and 0.31 MMT respectively.

The USDA’s Brazil and Argentina corn and soybean production estimates remain unchanged in the April WASDE. Brazilian corn and soybean production estimates were slightly less than trade expectations by 0.09 MMT and 0.11 MMT respectively. Argentinian corn and production estimates slightly outperformed expectations by 0.7 MMT and 0.21 MMT.

Initial Market Reaction

The immediate market reaction to the USDA reports saw corn prices immediately go from trading at $4.77 minutes before the report to $4.82 shortly afterwards. Within the hour, corn prices dropped back down to $4.79 before increasing to $4.84 at 1:00 om CST. May and July corn futures both immediately saw a 4 cent increase to $4.81 and $4.87 respectively. December corm futures decreased by 1 cent to $4.52 before increasing to $4.54 throughout the rest of the day.

Soybean cash price rallied 11 cents to $9.70. Before the release of the WASDE, May and July soybean futures traded as much as 5 cents lower on the day. After the WASDE report, May soybean futures recovered to close at $10.29 (up 16 cents on the day) and July soybean futures rose to $10.37 (up 13 cents on the day). November soybean futures traded in a 10-cent range around the report and closed up 7.75 cents at $10.0475.

May soybean meal prices slightly decreased by $1/ton to $295.20/ton before increasing to $297.60/ per ton later in the day. May soybean oil prices saw an initial decrease to 45.77 cents per pound before increasing throughout the day to 46.18 cents per pound.

May wheat futures initially decreased by 3 cents per bushel to $5.36. May wheat futures recovered to $5.40 before dropping back down to $5.37. July wheat futures followed a similar trend by decreasing by 3 cents initially to $5.51, then rose to $5.56 before dropping to $5.52 by mid-afternoon. September and December wheat futures also decreased by 3 cents initially before recovering and closing at $5.67 and $5.89 respectively.

Changes to Domestic Balance Sheets

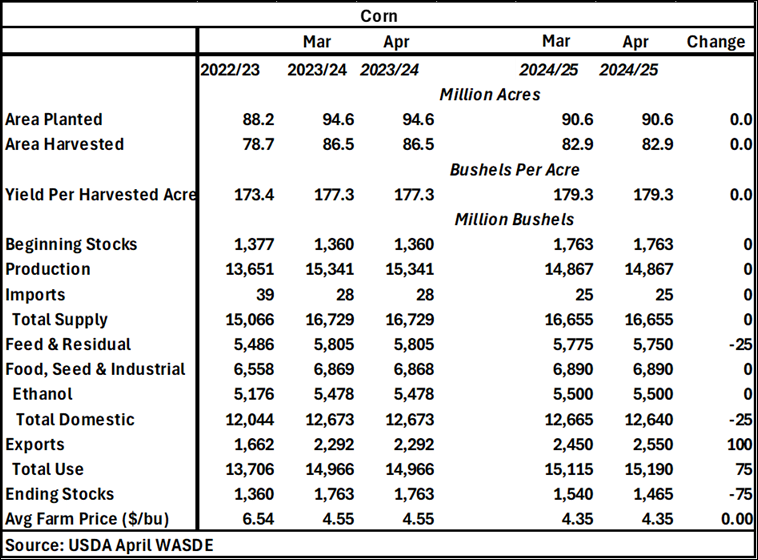

For corn, there were no changes in the 2023/2024 balance sheet. For the 2024/2025 balance sheet, US corn used in feed and residual decreased by 25 mb, resulting in a 25 mb reduction in total domestic. Exports increased by 100 mb, which leads to a 75 mb increase in total use when accounting for the 25 mb decrease in total domestic. As previously mentioned, US corn ending stocks decreased by 75 mb to 1,465 mb.

Table 2. April 2025 WASDE Corn Balance Sheet

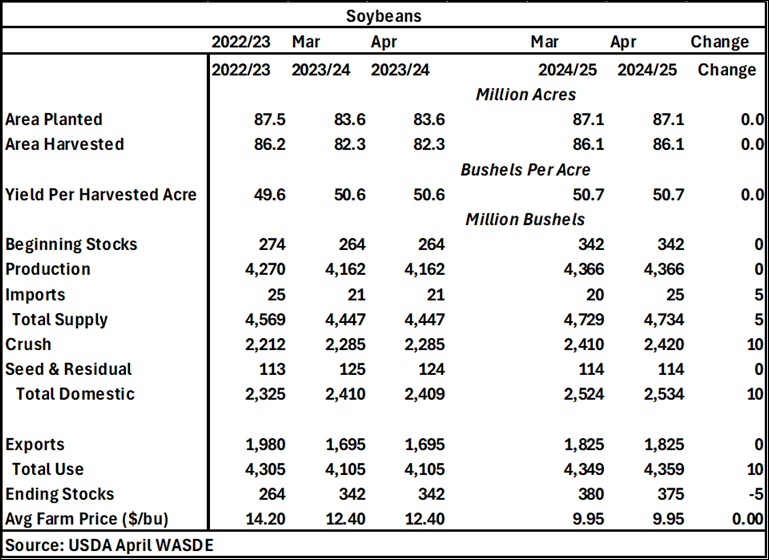

For soybeans, the only changes in the 2023/2024 balance sheet are a 1 mb decrease in seed and residual, leading to a 1 mb reduction in total domestic. For the 2024/2025 balance sheet, imports increased by 5 mb, resulting in a 5 mb increase in total supply. Crush increased by 10 mb, therefore total use also increases by 10 mb. US soybean ending stocks decreased by 5 mb to 375 mb in the April WASDE.

Table 3. April 2025 WASDE Soybean Balance Sheet

Want more news on this topic? Farm Bureau members may subscribe for a free email news service, featuring the farm and rural topics that interest them most!