Ag Sector Update - Federal Reserve Banks of Kansas City and Chicago

Author

Published

5/16/2023

Outlook

In a recent report by Nate Kauffman and Ty Kreitman of the Kansas City Federal Reserve bank, they indicated that agricultural credit conditions remain strong and farm real estate values continue to increase, but the growth rate in land values has softened. Strength in farm real estate markets eased, but farmland values continued to increase despite downward pressure from higher interest rates. Farm income moderated alongside a slight pullback in commodity prices during the first quarter slowing the pace of increase in loan repayment rates. While improvement in farm finances and credit conditions steadied and some lenders expected a degree of deterioration in the months ahead, multiple years of strong incomes continued to keep credit stress low.

The outlook for the U.S. farm economy in 2023 remains favorable overall as prices of some commodities hovered near multi-year highs and selected commodities such as fed cattle reached all-time highs. Elevated production expenses, higher interest rates and drought continued to present headwinds for many producers, but current commodity prices kept profit opportunities within reach. Higher production expenses pushed many producers to increase lines of credit, but others also pursued cost-cutting measures or utilized cash to reduce financing needs, dampening loan demand at many banks. Financial performance and liquidity at agricultural banks remained solid and farm lenders appeared well-positioned to meet higher credit demand through the early months of 2023.

Interest Rates and Farmland Values

Farm loan interest rates rose alongside further increases in benchmark rates. The average rate charged on agricultural loans was about 30 basis points higher than the previous quarter and nearly 300 basis points higher than a year ago (Chart 1). Farm loan interest rates climbed alongside increases in the federal funds rate and other key benchmarks and pushed credit expenses up considerably.

Growth in farm real estate markets has softened as interest rates have risen, but land values still continued to increase in the first quarter. The pace slowed from the rapidly accelerating growth in early 2022, but the value of agricultural land increased about 10% from a year ago. Cash rents on farmland have increased alongside growth in land values but steadied quickly in the first quarter.

David Oppedahl, the senior economist at the Federal Reserve Bank of Chicago which covers the Seventh District reports that land values in the first quarter of 2023 were up 10% compared to a year ago and “good” farmland values in the District rose 2% from the fourth quarter of 2022 indicating that even with increasing interest rates farmland values were still moving higher. Despite demand to purchase farmland still being up, there was a smaller amount of farmland for sale in the three- to six-month period ending with March 2023 than in the same period ending with March 2022. Moreover, the number of farms and the amount of acreage sold were down somewhat during the winter and early spring of 2023 compared with a year earlier. Annual cash rental rates for District farmland saw an increase of 8 percent in 2023—down from their gain of 11 percent in 2022.

Despite experiencing its smallest year-over-year gain (10 percent) in agricultural land values since the second quarter of 2021, the District still extended its streak of double-digit farmland value increases to eight quarters in the first quarter of 2023. Farmland values rose 2 percent in the first quarter of this year from the fourth quarter of last year (see table and map below). After being adjusted for inflation with the Personal Consumption Expenditures Price Index (PCEPI), the year-over-year gain in District farmland values for the first quarter of 2023 was 5 percent (the tenth consecutive quarter of real increases that were at least as large).

Cash rental rates for 7th District farm acres increased by 8 percent from 2022 to 2023, after rising somewhat faster (by 11 percent) from 2021 to 2022. For 2023, average annual cash rents for farmland were up 10 percent in Illinois, 2 percent in Indiana, 10 percent in Iowa, and 4 percent in Wisconsin.

Farm Income and Credit Conditions

The acceleration in farm real estate values also slowed alongside a moderation in farm income. About 40% of respondents reported that income was higher than a year ago and 25% reported that income was lower. The prices of some key commodities have retracted from historically high levels in recent months and production costs remained elevated, putting downward pressure on profit margins and tempering the outlook for liquidity and farm income.

Capital spending flattened quickly in recent quarters while household spending continued to grow more steadily. The pace of increase in farm borrower capital spending was measured, with 30% and 25% of banks reporting higher and lower spending compared with last year, respectively.

Strong farm income in recent years has bolstered borrower liquidity and continued to dampen loan demand at many banks. Non-real estate farm loan demand in the 10th District was less than a year ago at nearly 30% of reporting banks and higher at 20%. Despite some moderation in recent months, liquidity at agricultural banks remained sufficient to meet credit demands and 75% of respondents indicated availability of funds was unchanged from a year ago.

Elevated production costs have led many producers to cut costs or request credit line increases. According to respondents, many producers tried to reduce expenses by making changes or becoming more diligent about monitoring costs, and others have increased credit usage. Many borrowers also utilized cash reserves to reduce lending needs and interest expense as financing costs have also increased considerably alongside higher interest rates.

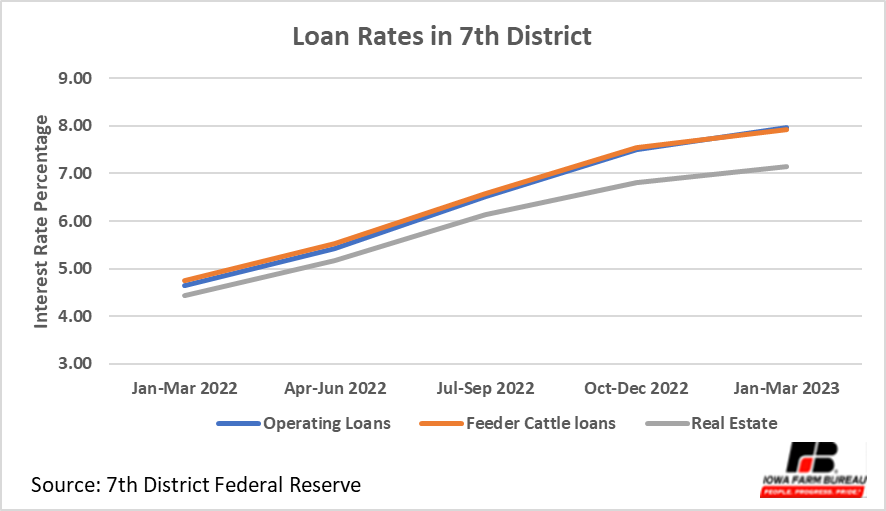

In the first quarter of 2023, agricultural credit conditions for the 7th District were once again in good shape, despite the jump in farm interest rates over the past year. As of April 1, 2023, the average nominal interest rates on operating loans (7.97 percent), feeder cattle loans (7.93 percent), and agricultural real estate loans (7.14 percent) were higher than at any time since the third quarter of 2007 (Figure 1).

The index of repayment rates for non-real-estate farm loans (123) indicated improvement for the tenth quarter in a row; 26 percent of responding bankers observed higher rates of repayment for the first quarter of 2023 relative to the first quarter of 2022, and 3 percent observed lower rates. Also, only 1 percent of the survey respondents reported higher levels of loan renewals and extensions over the January through March period of 2023 compared with the same period last year, while 15 percent reported lower levels of them. Yet, bankers reported a doubling to 2 percent, on average, of their farm borrowers having more carryover debt (loans not paid off at the end of the growing season and subsequently carried over into the next one) in 2023 than in 2022. The share of loans guaranteed by the USDA’s Farm Service Agency (FSA) in the portfolios of the reporting banks across the 7th District was just under 6 percent—nearly the same level as in the past several years.

Figure 1. Loan Rates in 7th District

Want more news on this topic? Farm Bureau members may subscribe for a free email news service, featuring the farm and rural topics that interest them most!